Most people spend more time picking a car colour than understanding their loan structure. But in 2026, with the Total Debt Servicing Ratio (TDSR) tightening and PARF rebates slashed, your financing strategy for getting a car loan (Singapore) is more important than the car itself.

This guide covers what actually matters before you sign anything: how much you can borrow, what the real cost looks like over time, and the mistakes that cost buyers thousands of dollars they didn’t need to spend.

What the MAS Rules Actually Mean for You

The Monetary Authority of Singapore (MAS) controls how much you can borrow when buying a car. The rules are based on the car’s Open Market Value (OMV).

Here’s the simple version:

- OMV $20,000 or below: You can borrow up to 70% (30% downpayment).

- OMV above $20,000: You can borrow up to 60% (40% downpayment).

- Maximum loan tenure: 7 years

These aren’t negotiable as every bank and licensed moneylender in Singapore has to follow them.

What this means in practice:

If you’re buying a used Honda Jazz priced at $51,800 with an OMV of $16,213, you can borrow up to $36,260. You’ll need a minimum downpayment of $15,540 — and that doesn’t include COE, road tax, or insurance.

If you’re buying a used BMW X3 priced at $188,888 with an OMV of $47,380, you can only borrow 60%, meaning you’ll need to come up with $75,555.20 upfront. That’s a number worth knowing before you fall in love with the car.

Check out our latest listings to see our quality inventory of petrol and hybrid models. We’ve also included a loan calculator at the bottom of the page so you can easily access your eligibility and run your own calculations instantly.

The 2026 “Silent Killer”: TDSR

Even if you have the 40% downpayment, the bank might still say no. Under the 55% TDSR rule, your total monthly debt (car loan + home loan + credit cards) cannot exceed 55% of your gross monthly income.

Pro Tip: If you have a large mortgage, your car loan eligibility might drop from 60% to as low as 30%. Always get a “Pre-Approval” before you fall in love with a car.

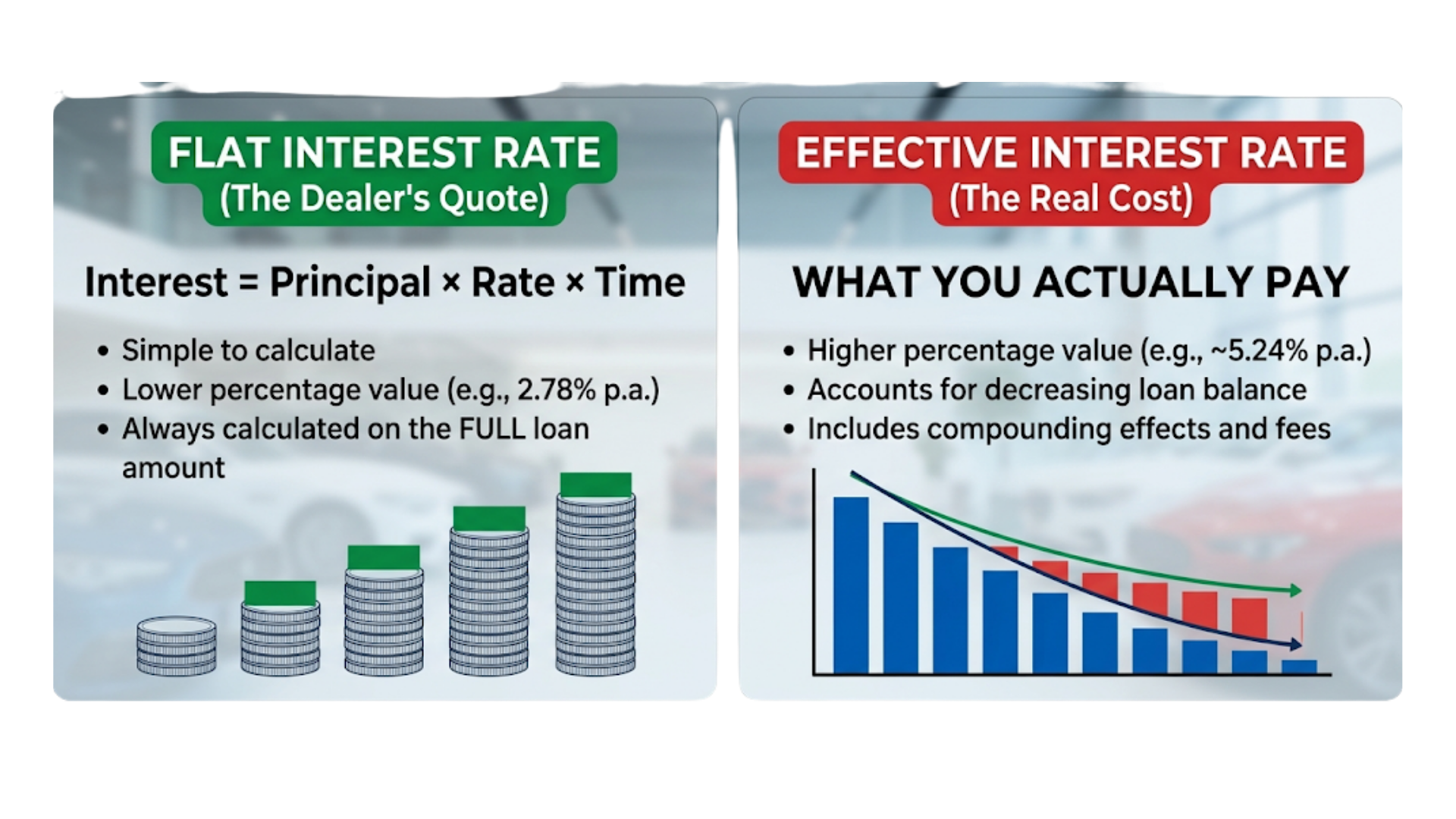

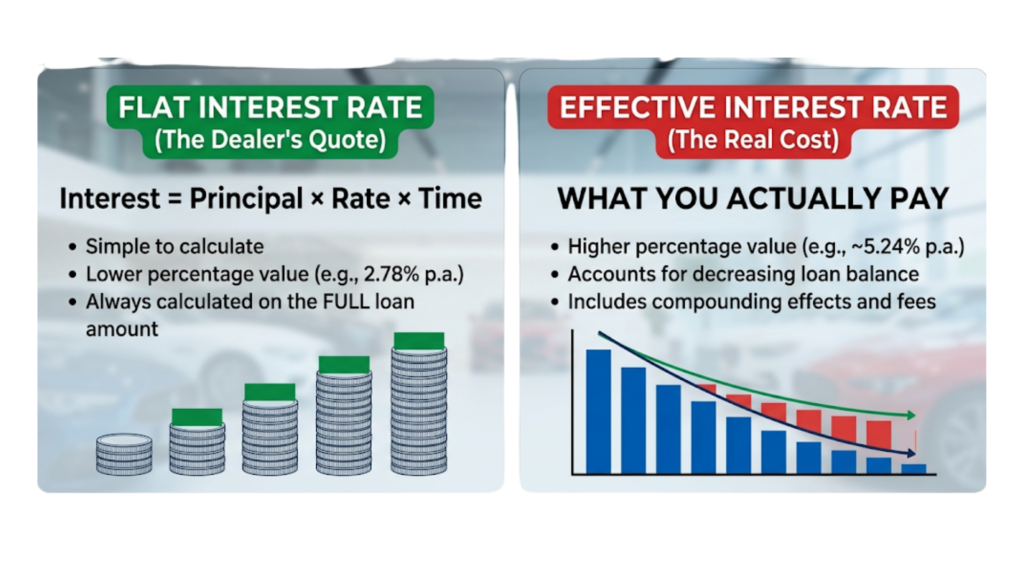

The Monthly Instalment: More Than Just Dividing the Loan

A common mistake is taking the loan amount, dividing by the number of months, and calling it a day. That’s not how it works.

Car loans in Singapore typically use a flat interest rate, not a reducing balance rate. This means interest is calculated on the full loan amount for the entire loan tenure — not just the outstanding balance.

Here’s a quick example:

- Loan amount: $35,000

- Flat interest rate: 2.78% per annum

- Loan tenure: 5 years (60 months)

Total interest paid: $35,000 × 2.78% × 5 = $4,865

Total repayment: $39,865

Monthly instalment: $664

That’s almost $5,000 in interest on a relatively small loan. On a larger loan, or over 7 years, the number climbs fast.

Vision Motoring’s loan calculator lets you model this instantly. Simply key in your loan amount, interest rate, and tenure to see the full picture before you commit.

How COE Affects Your Loan

Here’s something that catches a lot of buyers off guard: in Singapore, your car loan is calculated on the total purchase price which includes the COE component.

So if you’re buying a car with 5 years of COE left, a portion of what you’re financing is essentially the cost of that remaining certificate. When the COE expires (or when you choose to renew or de-register), that chunk of your loan doesn’t come back to you.

This is why COE tenure matters enormously when evaluating a used car.

A car with 9 years of COE left at $70,000 is often a smarter purchase than a car with 2 years of COE left at $40,000 — even though the monthly instalments on the cheaper car look lower.

The Budget 2026 “PARF Squeeze”

For years, buyers relied on a big “PARF rebate” check (50% of ARF) at the end of 10 years to fund their next car. That changed in February 2026.

- The Cut: PARF rebates were slashed by 45 percentage points. For cars registered after Feb 20, 2026, you now only get 5% of the ARF back at year 10.

- The Cap: Rebates are now capped at $30,000 (halved from $60,000).

What this means: Your car’s “future cash value” is significantly lower. You must factor this higher depreciation into your monthly budget, as you won’t get a large lump sum back when you scrap the car.

The Hidden Cost Most Buyers Forget: Insurance

Your bank will require comprehensive car insurance as a condition of the loan. This is not optional.

For a used car in Singapore, expect to budget:

- $1,200 to $2,800 per year for comprehensive insurance, depending on:

- Your age and driving experience

- The car make, model, and engine capacity

- Your No-Claims Discount (NCD) percentage

If you’re a young driver (under 27) or have a low NCD, insurance can be a significant annual cost — sometimes close to $3,000. Factor this into your total cost of ownership calculation before comparing loan instalments.

What You Should Actually Do Before Applying for Car Loan (Singapore)

1. Know your loan elibility.

Use this quick check:

| Step | Calculation |

| 1. Income | Your Gross Monthly Salary |

| 2. TDSR Limit | Multiply Income by 0.55 |

| 3. Existing Debt | Subtract Mortgage, Credit Card Min. Payments, etc. |

| 4. Max Car Loan | This is the maximum monthly instalment you can legally afford. |

2. Calculate the full picture, not just the monthly instalment.

Use Vision Motoring’s loan calculator to model different tenures and amounts. A 7-year loan lowers your monthly payment — but you’ll pay significantly more interest overall. There’s often a sweet spot around 5 years.

3. Ask about PARF and COE rebates.

If you’re de-registering your current car to fund the purchase, you’re entitled to PARF and COE rebates. This can be a meaningful source of upfront cash — and a good reason to time your purchase strategically.

Ready to run the numbers?

At Vision Motoring SG, we don’t just sell cars; we structure deals that make sense in the long run. Our team can help you calculate your exact TDSR and navigate the new 2026 PARF rules.

If you want to run the numbers on a specific car, our loan calculator takes about 60 seconds to use. Or WhatsApp us directly at +65 8957 0881 — our the team are happy to walk you through the financing options for any car in our inventory.

Your satisfaction, our vision.